I looked up the language for the lease we have on my wife's car. Keep in mind this is NOT through Kia, so the terms can be different.

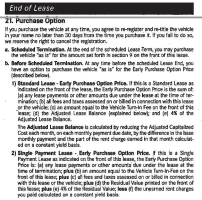

(c) Looks like Kia charges ~$400 for the vehicle turn in.

After reading (d) the Adjusted Lease Balance, it seems @Travis Wills and @Ruturaj are correct in that you don't need to pay the interest on the full term of the lease (just on the payments you already made).

BUT, check out (e) 4% of the Adjusted Lease Balance. So while you didn't pay the interest/money factor, you are paying a 4% fee on the total which could be like another $400 plus the turn in fee (so $800 total).

Then do you have to re-register it with the new lien holder?

I don't know, it seems like a lot of effort. Can you not just buy at the 0% interest Kia was offering at that price?

(c) Looks like Kia charges ~$400 for the vehicle turn in.

After reading (d) the Adjusted Lease Balance, it seems @Travis Wills and @Ruturaj are correct in that you don't need to pay the interest on the full term of the lease (just on the payments you already made).

BUT, check out (e) 4% of the Adjusted Lease Balance. So while you didn't pay the interest/money factor, you are paying a 4% fee on the total which could be like another $400 plus the turn in fee (so $800 total).

Then do you have to re-register it with the new lien holder?

I don't know, it seems like a lot of effort. Can you not just buy at the 0% interest Kia was offering at that price?