Let me start over.

Everything I've said before this was from a misunderstanding. The residual value plus remaining payments does not equal the buyout figure: it equals the buyout figure plus what you will save if you exercise the buyout now.

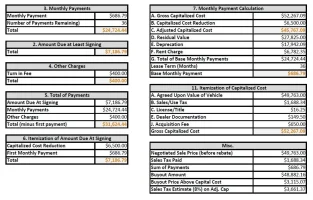

The buyout figure includes sales tax, and avoids all rent charge, just as Mach_Tuck has said all along. I talked to KMF in detail this morning and it is all clear (not clear as mud).

I will use my lease as an example (if you do this the instant your lease kicks in you get full savings; we have paid two additional months on ours, so we lost a bit of money, but not enough to get worked up over).

When we bought the Stinger, the dealer knocked a full $2,995 off MSRP up front. That's where dickering comes in. Where we live, Stingers are evidently in good supply and moderate demand.

Next up is the savings to us at the end of the 36 months of the lease: this is $4,293.47 that we will have kept back by exercising the buyout now: 33 more months of Rent Charge and the $400 reclaiming fee charged by the dealer (I don't know if the "option to purchase" is included in the buyout or not, but it's $300; in my figuring I am assuming that it is not included).

When you add up everything it is $7,288.47, or a savings on today's MSRP of 16%.

If I look at it as paying myself over seven thousand dollars for the trouble of selling the car, I think I can gird up my loins and do it!

")

Maybe I won't want to: maybe the 2018 Stinger will still be an awesome machine compared to the Stinger in three years. But if I lust after "new and better", I can sell and get a new lease, and do this all over again and save even more by getting the dealer to whack off even more from the MSRP, and avoiding any payments beyond the initial one.

The differences in paying off the buyout: If you can pay cash you of course avoid interest on financing the buyout. That is what we can do, this time. The savings if you finance the buyout will be less because you have to pay interest (currently c. 1.69% at the credit union; that's really friendly right now). The reason people lease is because they get a lower monthly payment. There is also an added security/benefit, called "gap insurance". KIA covers that when you lease. It's the difference between what your insurance company coughs up and the replacement value of a totaled car. Say my insurance pays off $21K of the residual; KIA will come up with the other $3,160.56.

So, now I know the hard numbers. I still have to assess the pros and cons. I still have to decide. But I am leaning toward exercising the buyout right now. I thought that I had decided to do it, but I still feel a question about it. "I'm reviewing, the situation ..."

")